“Only when the tide goes out do you discover who’s been swimming naked.” - Warren Buffett

Every major market cycle has a story that is at least partly true. In the late 1800s, railroads changed the world. At the turn of the 21st century, the internet changed the world. Today, technologies like artificial intelligence and companies like SpaceX may change the world. It’s human nature to innovate and move our species forward. Entrepreneurs imagine a future that does not exist yet, raise capital, take risks, and sometimes they build something extraordinary. That process is one of the best parts of capitalism. However, investors can get into trouble when they assume that every transformative technology makes every related investment attractive at any price.

There are countless investing philosophies on Wall Street, but one age-old concept feels especially

relevant today. In A Random Walk Down Wall Street, famed economist Burton Malkiel describes the

“castle-in-the-air” theory of investing. A towering castle viewed from afar can be beautiful, ambitious, and inspiring. In markets, that can look like a breakthrough technology, a visionary founder, or a new industry that could reshape the economy.

The key detail is that the castle is floating in the air. There is no foundation underneath it. In investing, that foundation is valuation, earnings, cash flow, margins, and realistic assumptions about future growth. When the story gets built too high above the fundamentals, the price starts to depend more on optimism than on what the business can reasonably support. The theory implies that an investment is only worth what the next person will pay for it, which starts to drift closer to speculation than investing.

Ben Graham, the father of value investing, made a similar point in a more practical way. He focused on price versus value and the need for a margin of safety. A business can be exceptional and still be a poor investment if the price already assumes too much of the future.

These theories intersect with today’s market and SpaceX. The company has changed the economics of space launch, built Starlink into a major satellite internet platform, and become strategically important across commercial, defense, and communications markets. The company is admirable, but the tricky part is figuring out what that future is worth today.

One way to put this valuation in context is through price-to-sales. SpaceX went public at nearly 100x price-to-sales, meaning investors were paying almost $100 for every $1 of sales. For another perspective, after its initial post-IPO rally in mid-June, SpaceX briefly surpassed the combined market values of JPMorgan and Walmart. An investment like that can work only if revenue grows rapidly, profit margins materialize, and the business eventually turns that growth into durable cash flow. The higher the starting price you pay, the more that needs to go right.

Source: Statista as of 6/11/26

This same idea applies to AI. At a recent family gathering, my brother, who is dipping his toes into investing, asked me a common question about AI and the buildout of data centers across the country: “Isn’t the demand basically infinite?”

Demand can be enormous and still fail to answer the investment question. A company still must build the product, fund the infrastructure, manage costs, compete with others, and earn an attractive return on the money it invests.

The late 1990s are a good reminder. The internet was real. Demand for data was real. In 1999, Wired noted that internet traffic was “doubling every 100 days,” which helped fuel the idea that the need for routers, fiber-optic cable, and telecom infrastructure could only move in one direction. That part of the story was directionally right, but many related investments still ended poorly. Too much capital chased the same obvious opportunity, capacity was overbuilt, prices fell, and the investment cycle became painful.

The Gartner Hype Cycle is useful because it shows how this pattern tends to play out. New technologies often move from early excitement to inflated expectations, then through a period of disappointment, and eventually toward more practical use. Expectations have a habit of moving faster than adoption, profits, and productivity.

Today’s AI buildout is already echoing that pattern. Microsoft CEO Satya Nadella, speaking about AI compute and energy needs, recently acknowledged that “there will be overbuild” and that because the message has gone out that companies need more energy and more compute, “everybody’s going to race.” That is the modern version of the telecom lesson. Demand may be real, but once the opportunity becomes obvious, capital can move faster than profits.

For now, the clearest AI winners have often been the companies tied to the buildout itself: semiconductors, data centers, power, infrastructure, and cloud computing. That has supported earnings and market leadership, but it also raises the bar. We are already seeing that shift from excitement to execution. Some large companies that rushed to put AI tools in employees’ hands are now setting usage caps, moving to cheaper models, or tightening budgets as the bills come in. Cost, reliability, and return on investment are starting to matter.

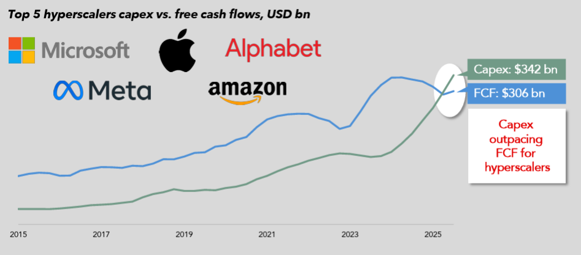

The broader market is now tied closely to this theme because the largest technology companies have become a much bigger share of the major indexes. For years, many of these companies were viewed as reliable free cash flow machines. Today, they are still highly profitable, but the AI buildout is consuming more cash, pushing capital spending higher, and leading some companies to rely more on debt issuance to fund data centers and infrastructure. When the largest companies in the index are spending more heavily, broad market exposure becomes more tied to one theme than it may appear.

Source: MUFG: Capital Markets Strategy, "The AI Chart Weekly" - 12/19/25

This is why bubbles do not have to show up only in stock prices. They can also show up in the assumptions behind the prices. If investors assume unusually high growth, margins, or demand, earnings expectations can become stretched too.

None of this means investors should be pessimistic about innovation or avoid technology altogether. Railroads and the internet changed the world, even though both also created market bubbles. The lesson from history is that the biggest stories often attract the most capital, and crowded opportunities can become more sensitive to disappointment when expectations are high.

The portfolio takeaway is simple. Diversification matters because no single theme should have to carry an entire portfolio. Valuation matters because even great companies can become less attractive when too much good news is already priced in. Rebalancing matters because it forces discipline when markets are rewarding the most exciting parts of the market. Investors can still participate in powerful trends without letting one narrative dominate the portfolio. That means diversifying across geographies, sectors and return drivers.

A castle in the air can look beautiful from a distance. Investing requires asking what is underneath it.